October 27, 2016

This is Part 2 of two-part series explaining thrv's process for executing Jobs Theory. Part 1 is about customer research you can do to define the right question that will drive your product development. This part is about answering that question.

If you've read Part 1 of this series, you know about the first 5 steps to executing Jobs Theory:

- Define your customer's jobs: functional, emotional, and consumption

- Identify all of the unmet needs in your customer's jobs

- Find the unmet needs

- Segment your customers

- Identify competitor weaknesses

This work leads to defining your question:

What can you do to serve your customer's unmet needs in the job better than the existing solutions?

The next step is to generate great product ideas that answer this question.

Step 6: Generate Ideas

You might have noticed something: in all the steps so far we haven't had any ideas. The traditional innovation process usually starts with product or solution ideas. An ideas-first process is fundamentally flawed because the goal of innovation is not to generate more ideas, it is to satisfy customer needs better than the existing solutions. Jobs Theory enables you to build a needs-first innovation process.

When I was a product manager at Microsoft in the 1990s, we had a "brainstorming" room where our team would go to spitball new ideas. Anything went. As you probably know, the only rule in brainstorming is "there are no bad ideas." This was (and is) absurd. There is a nearly infinite supply of bad ideas.

When executing Jobs Theory, you don't need to "brainstorm" because you have clear criteria to judge product ideas: the unmet customer needs in the job.

When you get your team together to generate ideas, start by writing an unmet need on the whiteboard. Then, ask the room: "What can we do to serve this need?"

It's still helpful for your team to think out of the box--perhaps your product is a website but a chatbot would serve the need much faster--but now, because you are answering a specific, measurable question, you know whether to keep the idea or move on.

If surgeons were your customers and you wanted to help them "restore artery blood flow," you'd ask about the unmet need, "Does the idea help surgeons reduce the likelihood of restenosis?"

If drivers were your customer and you wanted to help them "get to a destination on time," you'd ask "Does the idea help drivers reduce the time it takes to determine if an alternative route should be taken?"

If the ideas don't satisfy the needs, quickly move onto the next idea. If they do meet the needs, keep them on the list.

Push the team to build on the ideas and achieve step function improvements over the existing solutions. Don't let them be boxed in by the limitations of your existing product. The sky is the limit. Later, you can plan your roadmap to get there, step-by-step.

Now that you have a list of ideas that serve the unmet customer need, measure how well they do it--how much they improve the probability of achieving the goal as stated in the need.

Stack rank the ideas based on how much more reliably or faster they meet the needs than the existing solutions. If you see an idea that produces a step function improvement--reduces the time from days to hours, minutes to seconds, etc.--you may be sitting on a gold mine.

Jobs theory enables more efficient, precise, and relevant idea generation. Not only can you ensure all the ideas are relevant, but you can see if they are good enough.

Step 7: Price your product.

Pricing typically uses a combination of inputs, including the cost to make the product (or deliver the service), perceived value, and the price of substitute products in the market. Using this last input can be a fatal mistake for both pricing and market sizing.

To know why, you need to understand a pitfall of traditional market sizing: products and technologies come and go.

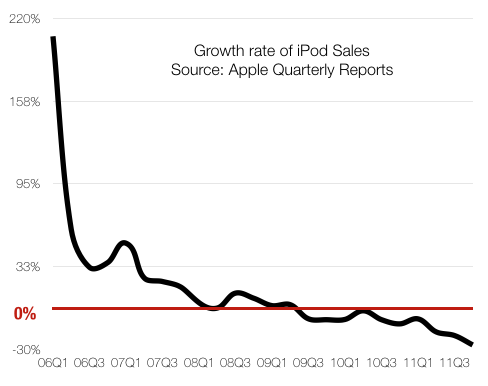

Traditional market sizing is based on variations of the following equation: the market = product price * the number of units sold. For example, in 2007 the iPod market was huge ($150 * 200 million iPods sold = $30 billion). Microsoft thought this was a big market and launched the Zune, an iPod competitor.

This is what the iPod market looked like at the end of 2011.

The "market" (defined by a product) went away, which means that Microsoft was looking to take a share of virtually nothing. But, of course, the true market, the customer's job-to-be-done, didn't go away. The iPod may have gone away, but people didn't stop executing the job.

Jobs Theory's definition of a market explains what happened.

There is no such thing as the "iPod" market. Customers don't want iPods anymore than they want records, cassettes, or CDs. What they want is to get a job done, i.e. create a mood with music.

"Price * units sold" is a flawed definition of a market because it can disappear from right under your feet. Defining the market based on the customer's job-to-be-done is much more helpful because the job will exist forever and therefore, the market will too.

To execute market sizing with Jobs Theory, you can look at the willingness to pay to get the job done. Willingness to pay can be measured by asking job executors (and if necessary purchase decision makers) how much it is worth to them to get the job done perfectly. The resulting data can be plotted (from high to low) on a line against the number of job executors. We call this a "need curve."

The area under the curve is the total market size. It will also identify the prices that will place your product at the high end of the market, the low end, or somewhere in between.

In Competing Against Luck, Clay Christensen says, "The reason why we are willing to pay premium prices for a product that nails the job is because the full cost of a product that fails to do the job -- wasted time, frustration, spending money on poor situations, and so on -- is significant to us."

By looking at the willingness to pay to get the job done, you can price your product to target the part of the market that will be the most profitable, and you can measure how lucrative that market will be over time, without the risk of it going away.

Step 8: Create messaging and positioning.

Positioning a product in a market and creating messaging that will resonate with customers is quicker and easier using the job-to-be-done and its customer needs.

When messaging misses the mark, it is usually because the message is focused on the product and its features. For example, Magellan messaged to potential customers that its RoadMate product has a "Wide-Angle Lens" and a "G-shock Sensor," both sophisticated technologies.

But how does a Wide-Angle Lens or a G-shock Sensor help a driver get to a destination on time? What need is it satisfying? If messaging describes the product features or technology, the customer has to figure out on their own how (and if) the features help them get the job done better.

Messaging based on satisfying the job-to-be-done is easier for customers to understand. And because the needs in the job-to-be-done are prioritized based on importance and satisfaction, you can create messages based on the most underserved customer needs in your market.

Step 9: Plan your roadmap.

"Jobs Theory enables innovators to make the myriad, detailed tradeoffs in terms of which benefits are essential and which are extraneous to a new offering."

--Clay Christensen, Competing Against Luck

The unmet needs in the job-to-be-done are your basis for making smart tradeoffs. Each job typically has about 100 customer needs. You can prioritize the needs by calculating the difference between the importance and satisfaction scores. The needs with higher importance and lower satisfaction are top priority. When you're choosing which product features to build now and which to postpone--making tradeoffs--you choose the features that meet the top priority needs.

The same mindset can be used to plan your road map. A great road map will balance cost, today's impact, and tomorrow's promise. During your idea generation, you may have come up with some brilliant ideas that will take a long time to build or be very expensive to execute. This doesn't mean you should ditch them. You just need to figure out how to increment your way to the brilliant idea while meeting customer needs better and better along the way.

This is step 1 of your road map planning: Determine the incremental improvements that will take you from where you are today to where you want to be tomorrow, getting the whole job done faster and more reliably than the existing solutions. Step 2 is to determine which of those incremental improvements to tackle first. The criteria for this prioritization is the extent to which the improvements serve unmet needs. You prioritize the work that tackles the most important and least satisfied needs.

Without good customer metrics, such as needs in the job-to-be-done, companies often prioritize their roadmap based on a flimsy projection of business impact, the charisma of people lobbying for the features they like, and the "HiPPO" (the Highest Paid Person's Opinion). All of these methods are subjective and/or based on unreliable premises.

Your product roadmap (and your tradeoffs) should not be prioritized by your team. They should be prioritized by your customer's unmet needs in the job.

Step 10: Mitigate your risk.

Understanding what causes a customer to purchase ("hire") a product can help you mitigate product development risk.

Competing Against Luck points out, "In 2015... one thousand publicly held companies spent $680 billion on research and development alone." And yet, "Most people would agree that the vast majority of innovations fall far short of ambitions, a fact that has remained unchanged for decades."

Once a product enters development, companies spend an enormous amount of capital, time, and resources on building, marketing, and selling the product. Jobs theory can help you avoid product failure and ensure the roadmap will generate the revenue and profit growth needed to justify the investment.

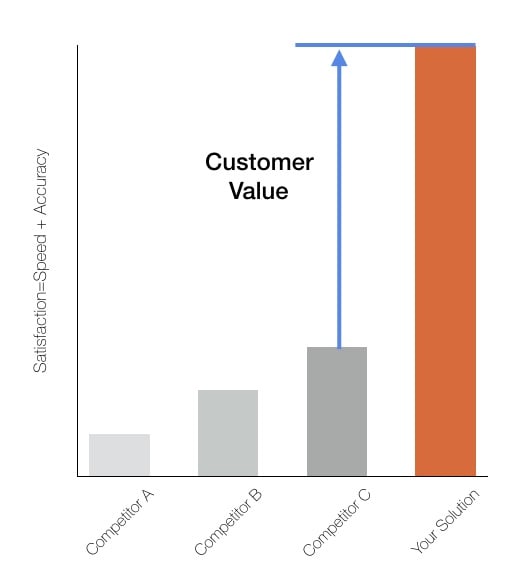

Failure occurs when a product does not create customer value in a market. What is "customer value?"

Customer value is a measure of the difference of customer satisfaction with getting the job done between your solution and the existing solutions. Since the goal is to satisfy customer needs and needs are metrics related to speed and accuracy, you can compare the speed and accuracy of getting the job done with your solution vs. a competitive solution. That difference is the customer value you've created.

Market opportunities exist because a person is struggling to get the functional job done. Improving the speed and accuracy of getting the job done reduces struggle and anxiety, which increases customer satisfaction and the likelihood they will hire your product.

This means you can measure the value of an idea even before you build it. Consider how much faster and more accurately your idea will meet the needs in the job if your idea is executed perfectly. Compare that to the baseline--the current satisfaction levels with each need in the job. You now know if the idea adds value to the market, so you've mitigated the risk of your idea. You still have execution risk, but your situation is a lot better than the risk of executing perfectly on an idea that does not add value in your market.

Step 11: Accelerate your growth.

Steps 1 through 10 are all the preparation steps to launching your product and accelerating your revenue growth. Jobs theory gives you a different lens through which to view your market, your customer, and your competition. It gives you powerful, metric-driven, customer-centric techniques to identify unmet needs and competitor weaknesses. And it gives you the tools to generate great product ideas that customers will pay for and to create messages that will resonate with customers.

Jobs theory is not easy to practice, but it is extremely effective if you make the organizational changes required to execute it well. As Clay writes, "Organizations typically structure themselves around function or business unit or geography -- but successful growth companies optimized around the job. Competitive advantage is conferred through an organization's unique processes: the ways it integrates across functions to perform the customer's job."

If you are interested in learning more about jobs-to-be-done techniques that you can use at your company, feel free to contact me directly.

Learn How to Grow Faster

Learn how to use JTBD to accelerate your growth and create equity value faster.